Shareholders of Houlihan Lokey would probably like to forget the past six months even happened. The stock dropped 21.1% and now trades at $139.43. This was partly driven by its softer quarterly results and may have investors wondering how to approach the situation.

Following the pullback, is now the time to buy HLI? Find out in our full research report, it’s free.

Why Are We Positive on HLI?

Founded in 1972 and known for its expertise in complex financial situations, Houlihan Lokey (NYSE:HLI) is a global investment bank specializing in mergers and acquisitions, capital markets, financial restructurings, and valuation advisory services.

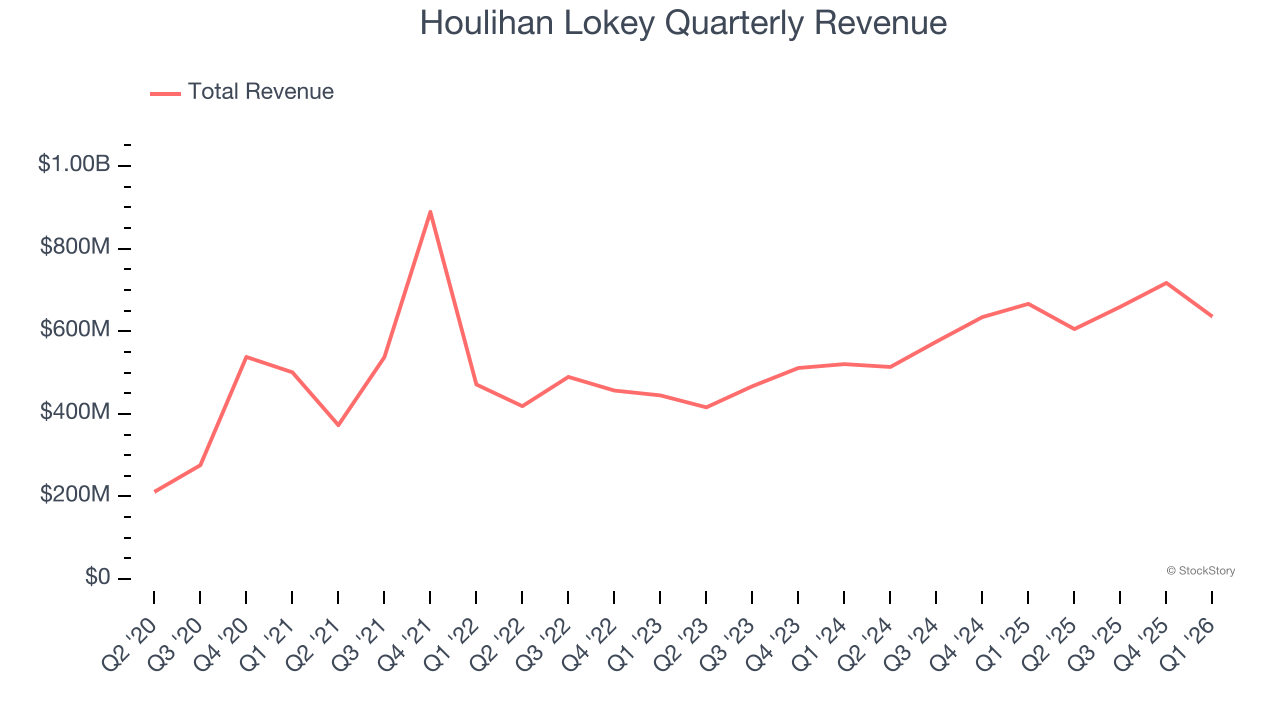

1. Long-Term Revenue Growth Shows Strong Momentum

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

Thankfully, Houlihan Lokey’s 11.4% annualized revenue growth over the last five years was solid. Its growth beat the average financials company and shows its offerings resonate with customers.

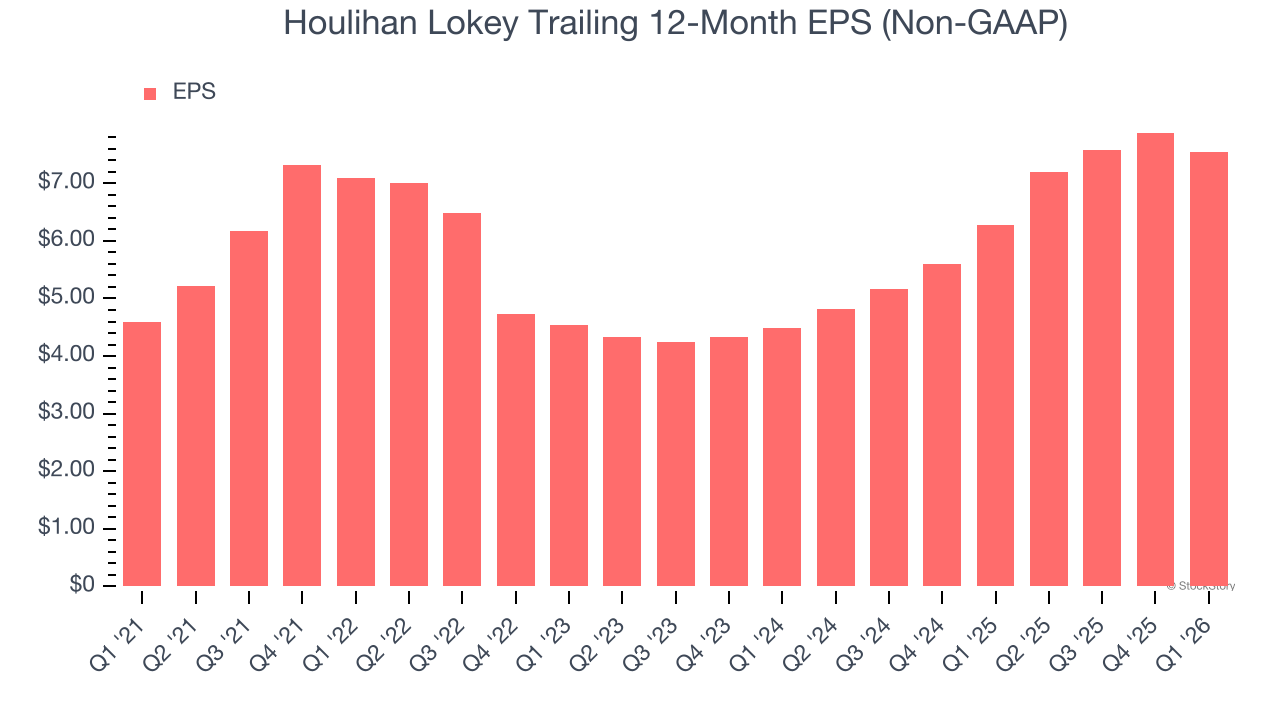

2. EPS Moving Up Steadily

Analyzing the long-term change in earnings per share (EPS) shows whether a company’s incremental sales were profitable — for example, revenue could be inflated through excessive spending on advertising and promotions.

Houlihan Lokey’s decent 10.5% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

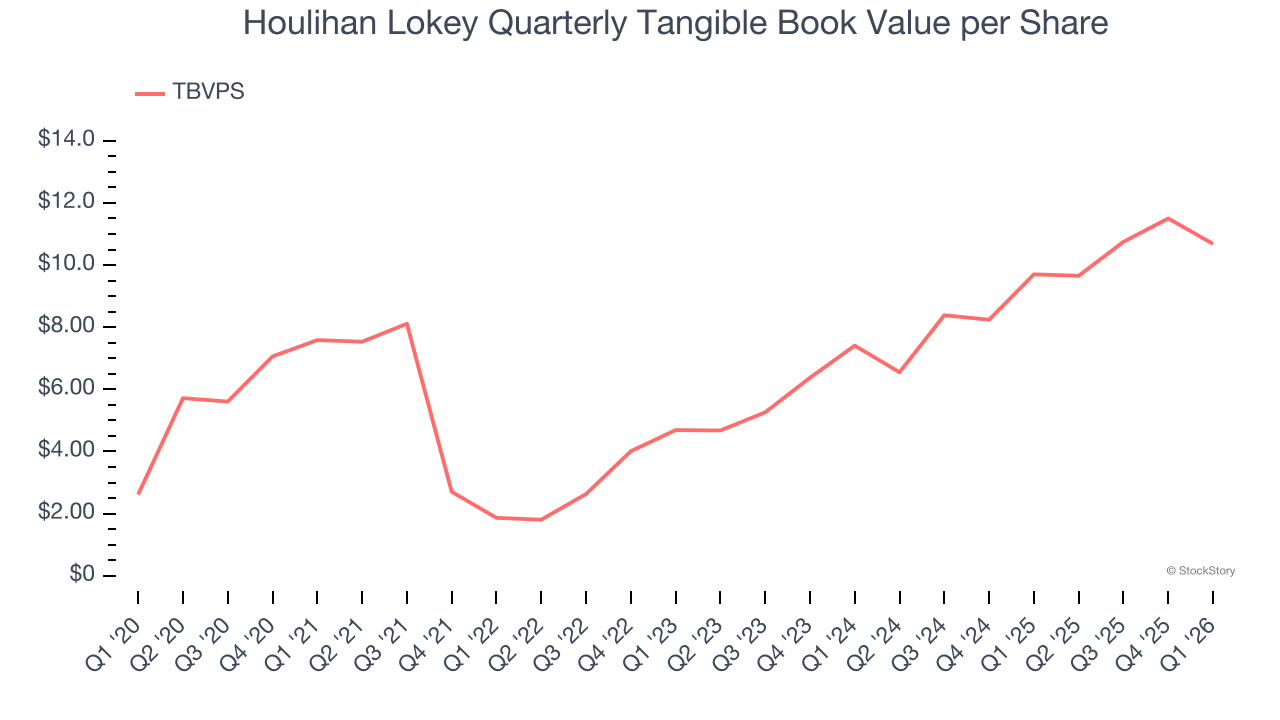

3. Growing TBVPS Reflects Strong Asset Base

Tangible book value per share (TBVPS) serves as a key indicator of a financial institution’s strength, representing the hard assets available to shareholders after removing intangible assets that could evaporate during economic distress.

Although Houlihan Lokey’s TBVPS increased by a meager 7.1% annually over the last five years, the good news is that its growth has recently accelerated as TBVPS grew at an incredible 20.1% annual clip over the past two years (from $7.41 to $10.68 per share).

Final Judgment

These are just a few reasons Houlihan Lokey is a high-quality business worth owning. With the recent decline, the stock trades at 17.2× forward P/E (or $139.43 per share). Is now the right time to buy? See for yourself in our in-depth research report, it’s free.

High-Quality Stocks for All Market Conditions

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren’t just high-quality businesses. Something is happening with them right now. Elite fundamentals meet near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week’s Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.